How Easy Is It To Report A Suspicious Investment Platform? We Tested ‘Top’ Regulators

We found a live investment platform with multiple suspicious red flags and went to report it to six global regulators on the same day. Our aim was to understand how easy it really is to report concerning financial firms, and how quickly some of the most trusted regulators actually act on such reports.

Christian Harris

Christian is a seasoned analyst, leveraging his expertise in stocks, forex, and crypto to evaluate brokers worldwide. With hands-on trading experience and a strong focus on risk management, he helps traders find reliable platforms. Christian's work for BrokerListings.com has been cited in the Financial Times.

Christian Harris Profile PageWilliam Berg

William Berg combines his expertise in law and finance to analyze trading brokers. He has checked 3,250+ regulatory licenses, investigated 2,365+ broker clones and trading scams, and placed 3,500+ trades.

William Berg Profile PageJames Barra

James is an experienced broker analyst with a background in financial services. He has spent 2,500+ hours testing brokers, used 35+ different platforms and apps, audited 120+ broker T&Cs, and verified 300+ regulatory licenses. James has also been on US and UK TV news channels discussing reports conducted by BrokerListings.com and sharing his expertise.

James Barra Profile PageJuly 13, 2026

In 2025, Americans reported $8.65 billion in investment fraud losses, according to the FBI’s Internet Crime Complaint Center. In the UK, investment scam losses reached £97.7 million in the first half of 2025 alone, according to UK Finance data. Australia lost $2.18 billion to scams across all types in 2025, with investment scams accounting for $837.7 million, according to the National Anti-Scam Centre and ACCC.

But here’s the number that should concern everyone: research cited by the Consumer Federation of America found that only 14% of financial fraud victims report incidents to authorities. This means roughly 86% never file a formal report.

Not because they don’t want to. Because most people have no idea where to start – and when they try, the process is slow, confusing, and rarely leads anywhere visible.

We wanted to test that firsthand. So we found an investment platform with multiple hallmarks that are highly suspicious, and reported it to six major regulators. We timed every step, documented every click, and scored each one.

What we found wasn’t surprising. But it was still frustrating.

Make Full WidthKey Takeaways

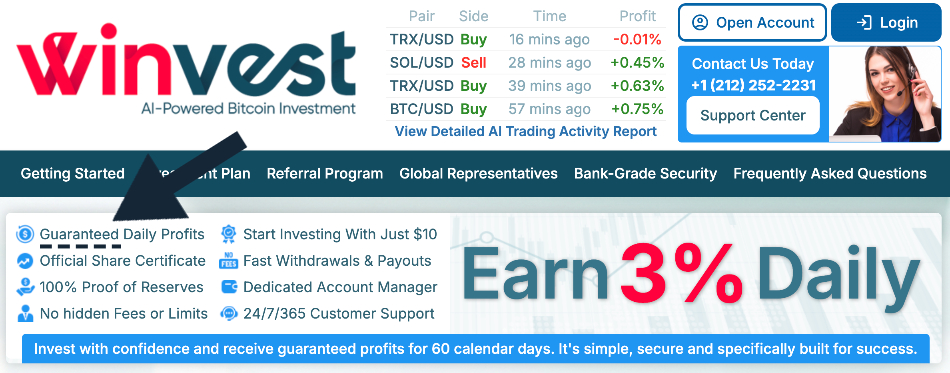

- In our opinion, online investment service, Winvest (https://winvest.com/), may be operating a misleading financial scheme, or at the very least is not authorized by trusted financial regulators. We documented 10 specific red flags.

- Warning signs included “guaranteed” 3% daily returns, an implied 1,095% annual return, claims of $105bn+ in withdrawals and 10m+ users, concerning tactics like “limited-time” urgency, Bitcoin-only deposits, and YouTube testimonials with comments disabled, plus no regulatory authorization.

- We reported our concerns to six regulators on the same day: UK FCA, US SEC, US CFTC, Australia ASIC, Cyprus CySEC and Singapore MAS. These are all ‘Category A’ bodies in our regulator classification system.

- We scored every regulator from 1 to 10 in 6 categories (ease of finding the report page, form simplicity, time to complete, confirmation/acknowledgment, response time, outcome or visible action). We also assigned an overall score before ranking regulators from the best to worst.

- The SEC scored highest at 47/60. The FCA scored 40/60, CFTC 35/60, and CySEC 29/60. MAS and ASIC reporting functionalities weren’t good enough to let us fully report the platform we were concerned about.

- Worryingly, no regulator has taken visible public action in response to our reports by the time of this report publication – no warning-list entry, investor alert, or meaningful follow-up. If they do, we will update this report.

- The delay is what’s most worrying, as research on wider scams, notably phishing links, found that 71.4% stopped operating within 30 days. While not purely focused on investment scams, this research helps show why slow reporting systems can leave regulators acting after most of the damage is done, and key evidence has disappeared.

- The biggest gap is cross-border reporting. Offshore or foreign-entity platforms can target users globally while leaving ordinary consumers unsure which regulator even owns the problem, likely leading many victims to give up as they hit border red walls.

- We put our concerns to Winvest via telephone (no answer) and their support email, giving them an opportunity to respond. Should they reply, we will update this report where appropriate.

| Regulator | Action visible by publication | Minutes to submit | Findability (/10) | Form simplicity (/10) | Completion speed (/10) | Confirmation (/10) | Response time (/10) | Visible outcome (/10) | Total | Grade |

|---|---|---|---|---|---|---|---|---|---|---|

| US SEC | No* | 7m 44s | 9 | 8 | 8 | 9 | 7 | 6 | 47/60 | A |

| UK FCA | No* | 2m 50s | 5 | 6 | 9 | 10 | 9 | 5 | 44/60 | B+ |

| US CFTC | No* | 10m 15s | 6 | 5 | 5 | 7 | 6 | 5 | 34/60 | C |

| Cyprus CySEC | No* | 5m 20s | 4 | 5 | 6 | 6 | 5 | 4 | 30/60 | C– |

| Singapore MAS | No direct MAS report completed** | N/A | [score] | N/A | N/A | N/A | N/A | N/A | 6/40 | N/A |

| Australia ASIC | No direct ASIC report completed*** | N/A | [score] | N/A | N/A | N/A | N/A | N/A | 4/40 | N/A |

*No visible public action had been taken by the time of publication. We checked whether the platform appeared on the relevant public warning or investor alert lists and whether we had received any meaningful follow-up from the regulator.

**MAS does not operate a direct consumer scam reporting form. Users are directed to the Singapore Police Force or ScamShield, so MAS could not be fully scored on the reporting journey.

***ASIC redirected international reporters away from its own reporting process before a report could be completed. Australian scam reporting is split between ASIC and ScamWatch, depending on the issue.

The Concerning Platform We Found: Winvest (winvest.com)

We didn’t have to look far. The platform we identified – Winvest, operating at https://winvest.com/ – was sitting in plain sight, running active social media promotions, appearing on HYIP (High Yield Investment Program) monitoring sites, and using terminology like “guaranteed daily profits” that is not permitted in many tightly regulated jurisdictions.

No legitimate or regulated investment service can guarantee profits

Why Winvest Looks Suspicious: 10 Red Flags

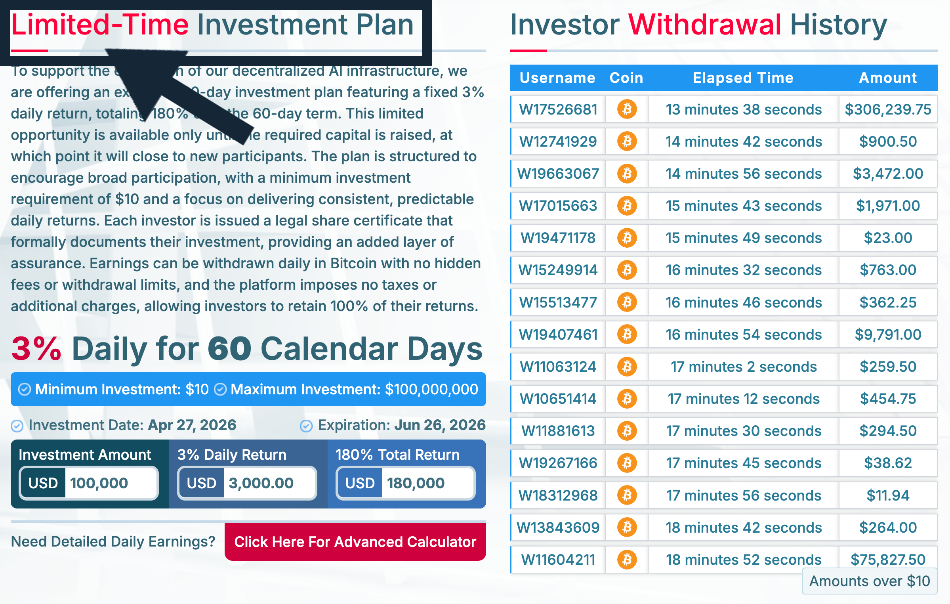

Red Flag #1: The Maths On Their Returns Doesn’t Work

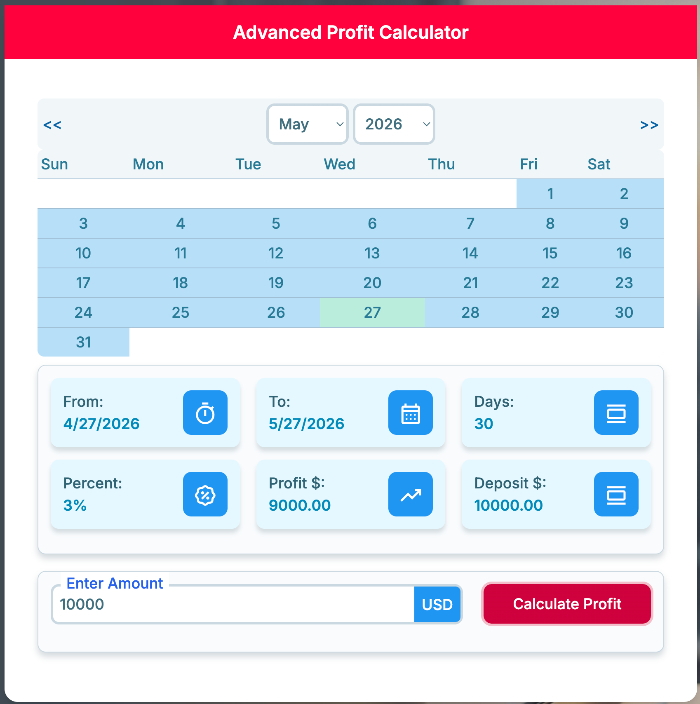

Winvest advertised a fixed 3% daily return, totalling 180% over 60 days. That sounds appealing until you run the numbers properly. A 3% daily return equals approximately 1,095% annually without compounding. With daily compounding, a $1,000 investment would theoretically grow to around $48.5m in a year.

No legitimate, regulated investment product on Earth has ever delivered anything close to that consistently. For context, the S&P 500’s long-term average annual return is approximately 10%. Winvest claims to deliver returns roughly 100 times higher each year, with “no” risk.

“Advanced” profit calculator helps suggest highly unlikely returns

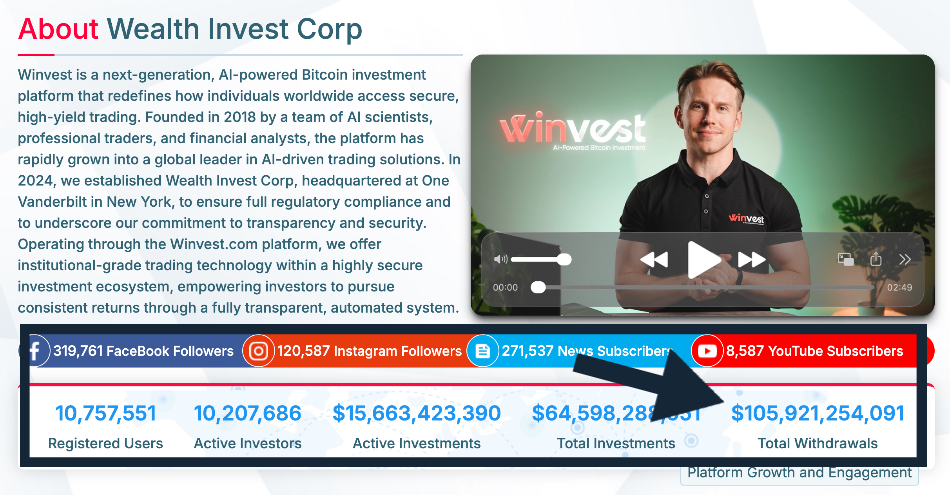

Red Flag #2: The $105 Billion Withdrawal Claim

At the time of our study, Winvest’s website claimed $105,761,663,274 in total withdrawals. That’s over $105 billion. If that figure were true, Winvest would be one of the largest financial platforms on the planet – larger than most sovereign wealth funds and comparable to a mid-tier global bank in terms of client assets processed.

And yet there is zero mention of Winvest in any mainstream financial publication – Bloomberg, Wall Street Journal, Financial Times, Reuters, or otherwise (we checked). A firm that has processed $105 billion in client withdrawals would make the front page of financial news.

Implausible withdrawal claims

Red Flag #3: “Limited-Time” Pressure Tactics

Winvest’s website stated the 60-day plan is a “limited opportunity” available “only until the required capital is raised, at which point it will close to new participants.”

This is a textbook urgency tactic. It pressures potential investors to deposit quickly, before they’ve had time to do due diligence. Most legitimate, regulated investment products don’t come with countdown clocks.

Urgent sales tactics deployed

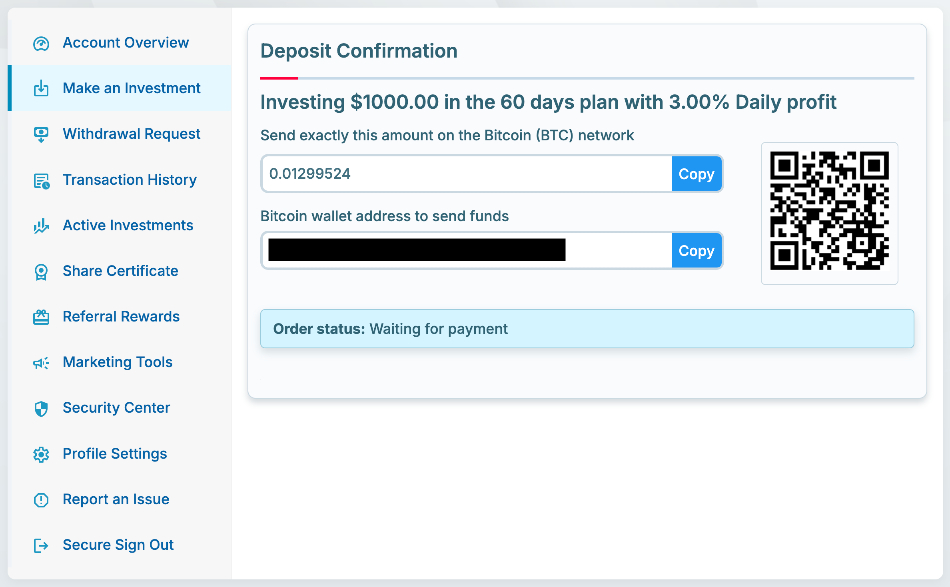

Red Flag #4: Bitcoin-Only Deposits

Winvest accepts deposits exclusively in Bitcoin. A firm claiming to be headquartered at One Vanderbilt in New York – one of Manhattan’s most prestigious office addresses – does not offer wire transfers, ACH payments, or standard banking deposits. Bitcoin transactions are effectively irreversible and can be difficult to trace once funds move through multiple wallets.

Unregulated platforms like Winvest are anonymous and can disappear at any time without notice. Bitcoin-only deposits are a structural feature that makes recovery almost impossible if things go wrong.

Winvest encourages crypto deposits and withdrawals

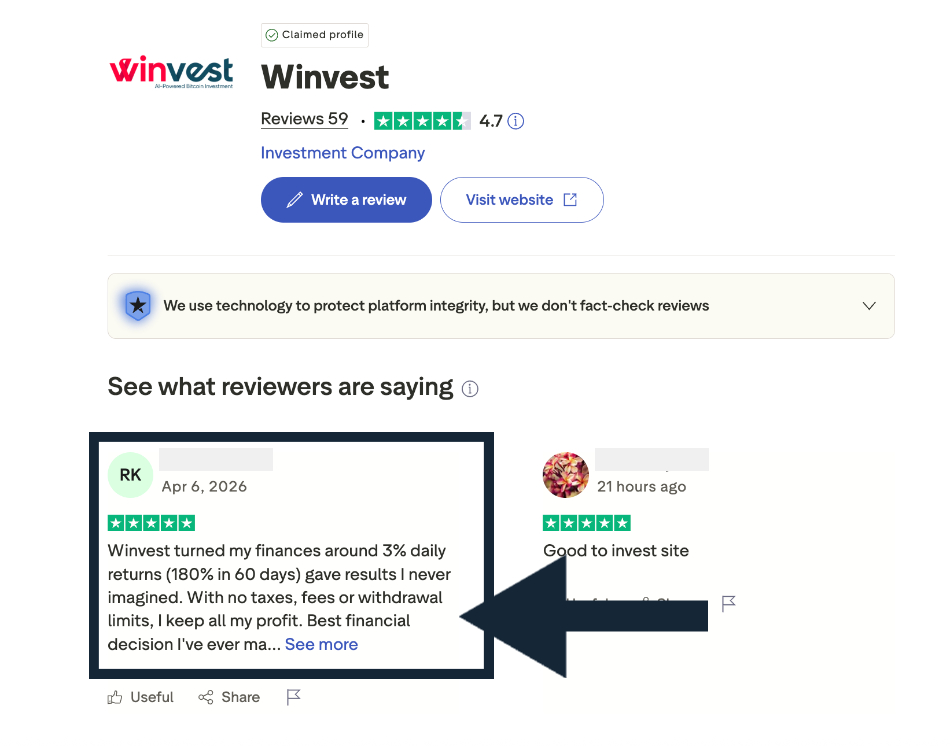

Red Flag #5: Suspicious Trustpilot Reviews

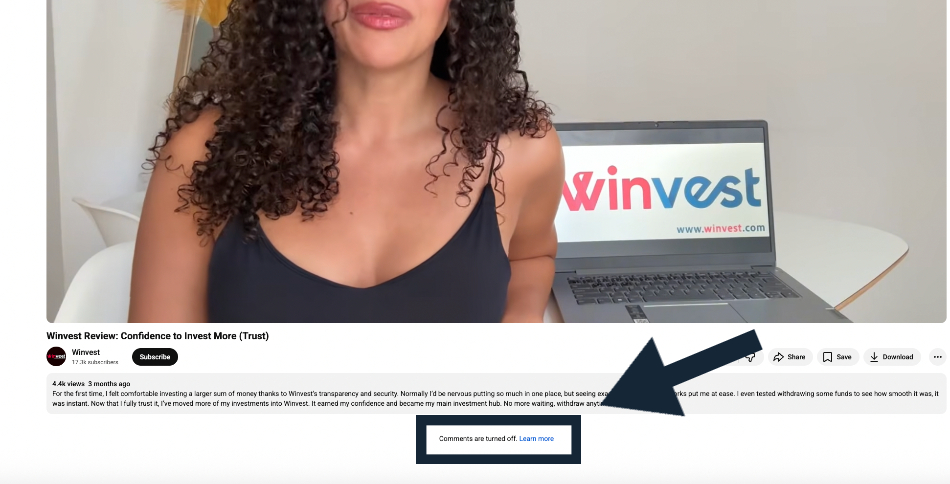

Winvest has only a small number of reviews on Trustpilot (just 34 at the time of our latest checks as Trustpilot “removed a number of fake reviews” ), but those remaining are still overwhelmingly positive – and the pattern is interesting. Multiple reviews follow an almost identical template, praising “3% daily returns (180% in 60 days)” in near-identical language, with phrases like “best financial decision I’ve ever made” and “life-changing website” appearing repeatedly.

This is consistent with what’s called “seeding” – paying early users (using deposits from newer users) to generate positive testimonials that build false confidence. A review base where every positive review praises the exact same percentage return is a significant pattern to note.

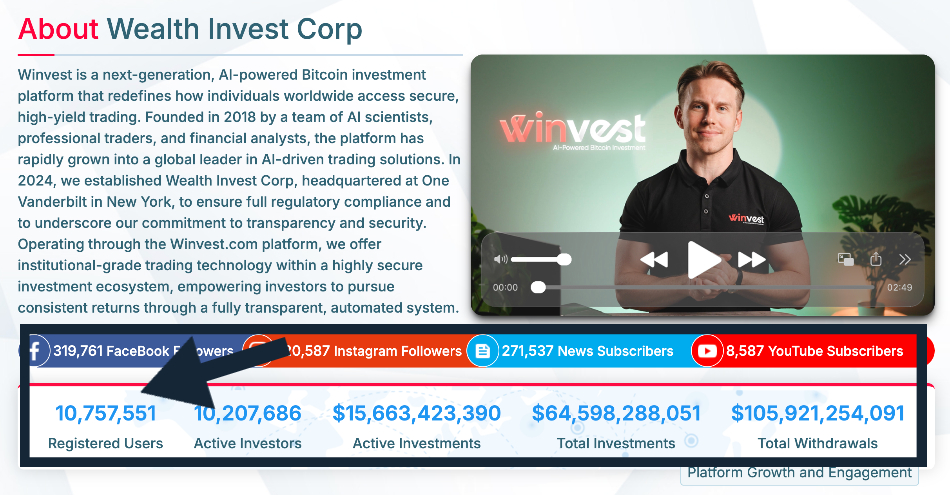

Red Flag #6: The 10m+ Users Claim Has No Footprint

Winvest claims to have over 10 million registered users. A platform with that many users would often have a substantial presence on third-party sites — forums, Reddit discussions, app stores, news coverage, and regulatory filings. A search across all of these yields very little in organic results.

The reviews available are typically either on HYIP monitor sites (which track high-risk, typically short-lived investment programs) or on review platforms whose content looks templated.

Winvest’s platform growth numbers are unlikely

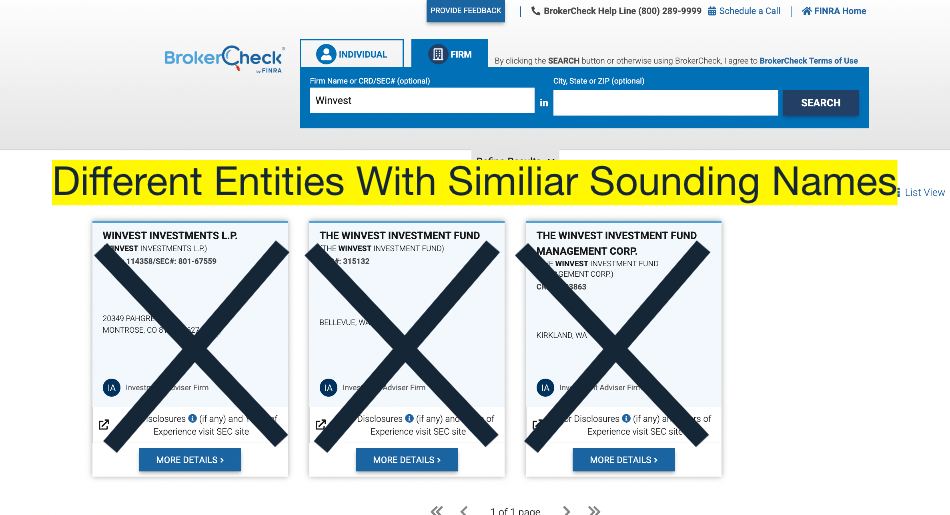

Red Flag #7: No Regulatory Registration

Winvest does not hold any valid regulatory certificates and is not regulated by any recognized financial authority. We checked FINRA’s BrokerCheck and the SEC’s EDGAR database for both “Winvest” and “Wealth Invest Corp” – their stated New York entity. Neither returned a match that was the firm in question (they returned some firms that sound similar but are different outfits. It’s possible the Winvest platform we’re concerned about is trying to imitate established current or historical companies).

The firm behind the platform, officially known as Longo Elía Bursátil S.A., is based in Argentina and is not regulated by any recognized financial authority. Their stated New York address – 224 West 35th Street, Suite 500 – is a virtual office, a common feature of companies that want a prestigious US address without a genuine US presence.

No match for the Winvest platform in question

Red Flag #8: YouTube Testimonial Videos With Comments Turned Off

Winvest hosts a series of video testimonials on YouTube, featuring individuals praising the platform’s returns and ease of use. At the time of our reporting, every single one of those videos had comments disabled. This is not a minor detail. On most legitimate and trusted financial platforms, user testimonial videos attract organic comments – questions, skepticism, follow-ups, competing experiences.

Disabling comments on promotional content may be a deliberate choice to prevent exactly that. It means the narrative can only flow one way. There’s no way to ask the “investor” in the video whether they actually received their money, no way to flag inconsistencies, and no way for potential victims to see warning signs left by others. Combined with every other red flag documented here, it’s a controlled information environment – one that benefits the platform, not its users.

Why does Winvest not want anyone to comment publicly on its videos?

Red Flag #9: Contradictory Corporate Identities

Winvest presents multiple conflicting versions of its own corporate identity. The platform claims to have been founded in 2018. It also states that in 2024, it established “Wealth Invest Corp” at One Vanderbilt in New York – one of Manhattan’s most prestigious and expensive office buildings.

Simultaneously, our research identifies the legal entity behind the platform as Longo Elía Bursátil S.A., incorporated in Argentina, with no connection to any New York-registered company. The New York address – 224 West 35th Street, Suite 500 – is a virtual office used by hundreds of unrelated firms.

A legitimate financial company doesn’t typically have three different founding narratives, two contradictory headquarters, and a legal entity that doesn’t match anything it publicly claims. This kind of layered, inconsistent identity is a structural feature of operations designed to be difficult to trace.

There is conflicting company details across Winvest’s materials

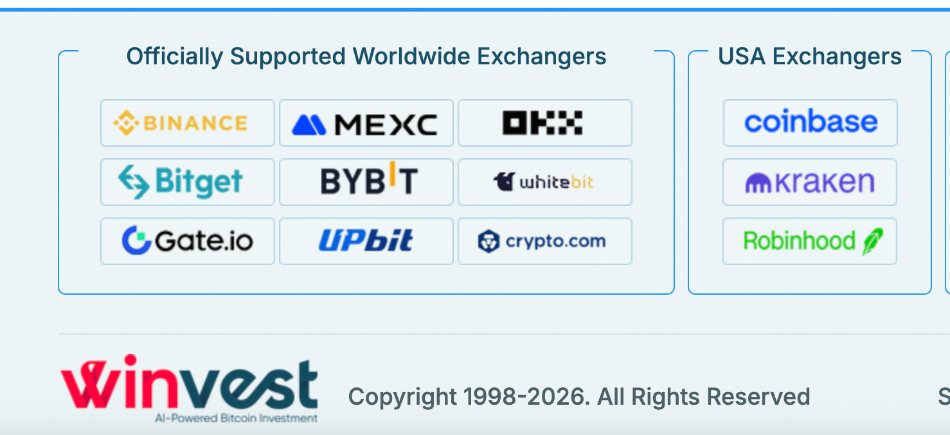

Red Flag #10: Unverified Exchange Partnerships

Winvest’s website lists the logos of Coinbase, Binance, Bybit, and Crypto.com – implying they are official partners or liquidity providers. We checked the official partner pages and announcements from each of these exchanges. None of them lists Winvest as a partner.

Legitimate exchange partnerships are formally announced, press-released, and verifiable through official channels. If a firm displays exchange logos without a genuine relationship, it is straightforwardly misleading to investors.

Winvest claimed exchange partners

While we have identified significant red flags in our investigation of Winvest, most notably around its promised returns and lack of regulatory authorizations, we cannot categorize this platform as fraudulent or a scam with certainty. This is a judgement that must be made by one of the regulators we’ve reported this firm to.

Methodology: How We Ran The Test

We screenshotted and documented all of the above – the website claims, the returns calculator, the Trustpilot review pattern, the YouTube videos, the FINRA/SEC search results – and compiled this into a single evidence package submitted identically to each regulator.

On the same day, at the same time, we filed an identical report with all six:

- FCA (UK) – Financial Conduct Authority

- SEC (US) – Securities and Exchange Commission

- CFTC (US) – Commodity Futures Trading Commission

- ASIC (Australia) – Australian Securities and Investments Commission

- CySEC (Cyprus) – Cyprus Securities and Exchange Commission

- MAS (Singapore) – Monetary Authority of Singapore

Each regulator was scored out of 10 across six criteria:

Make Full Width| Criteria | Question |

|---|---|

| Ease of finding the report page | Could a non-expert locate it without a search engine? |

| Form simplicity | Was the language and structure accessible to a general consumer? |

| Time to complete | Total minutes from landing page to submission |

| Confirmation/acknowledgment | Did we receive a reference number or formal receipt? |

| Response time | How long before any meaningful contact back? |

| Outcome or visible action | Any evidence the report led to a result? |

The Regulator Scorecards

FCA (Financial Conduct Authority)

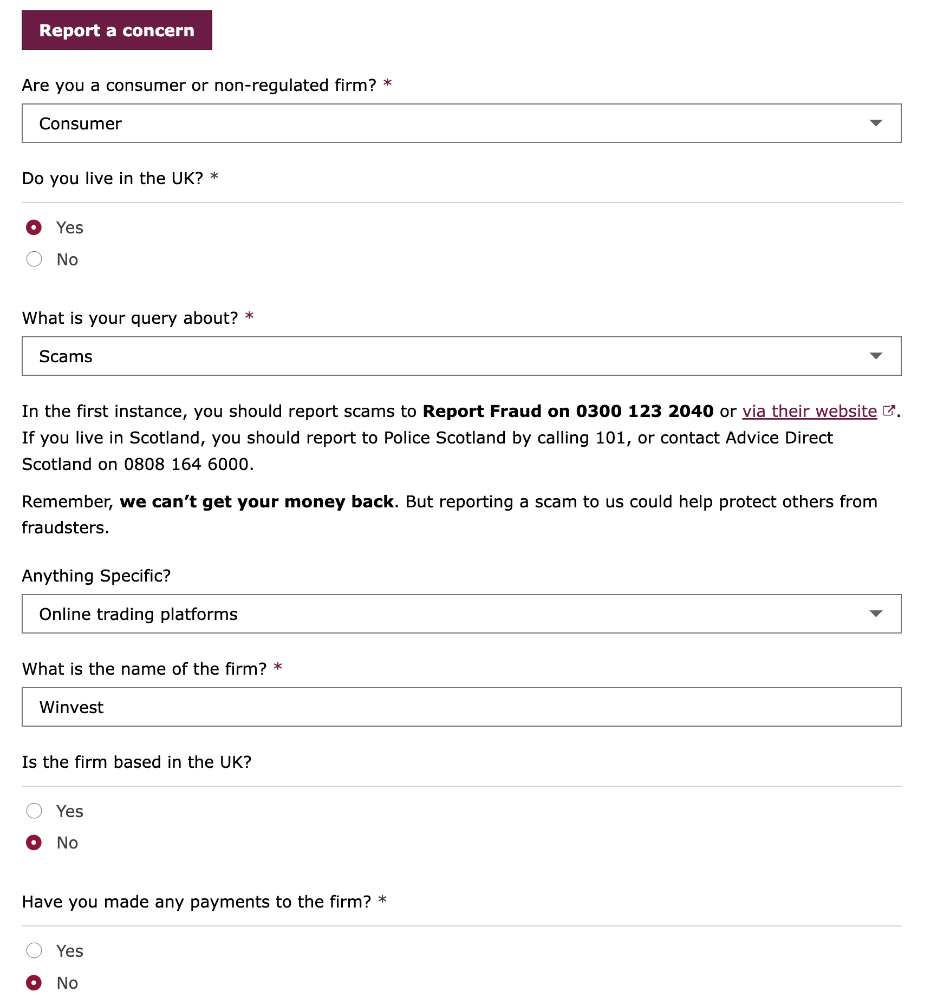

The FCA’s reporting function isn’t where you’d expect it. Searching “report a scam FCA” on Google gets you there faster than navigating the FCA website directly. From the homepage, it takes three menu levels before you reach the scam reporting form.

The form itself asks for your personal details, information about the scam, and the company name. There’s no anonymous reporting option. If you’re a victim who’s embarrassed or a whistleblower with a reason to stay private, that’s an immediate barrier. There’s also an option to attach a screenshot to the form – you can email them separately, but the link to do so is buried in a follow-up email.

FCA reporting form

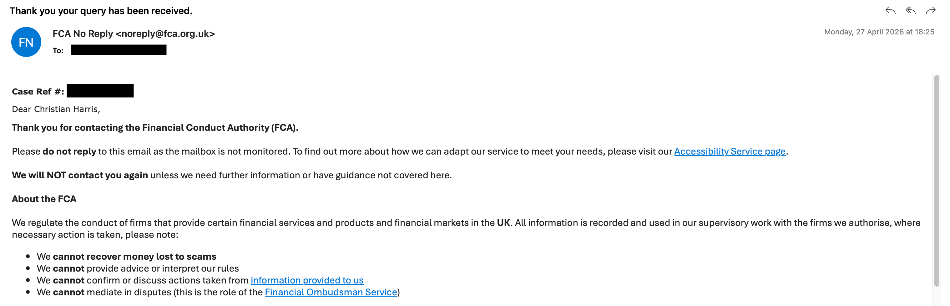

We received an automated acknowledgment via e-mail (we declined phone contact) within around 2 minutes, including a case reference number.

What happened to Winvest? We checked the FCA Warning List. As of the time of publication, it had not appeared on it, despite the platform promoting itself to UK users and accepting Bitcoin deposits without FCA authorization.

This is important because scam infrastructure can disappear quickly. Kaspersky found that 71.4% of monitored phishing links stopped showing signs of phishing activity within 30 days. While not focused only on suspicious financial platforms it still highlights the problem – if a reported firm takes weeks to appear on the Warning List, it stays operational during the window when it’s most dangerous.

SEC (Securities and Exchange Commission)

The SEC’s Tips, Complaints and Referrals (TCR) portal is genuinely the best-designed consumer-facing reporting tool we tested. It’s clearly linked from the homepage, loads quickly, and guides you through a 7-step logical category selection. Crucially, anonymous reporting is allowed – you can submit without giving your name.

The form has granular dropdowns covering investment fraud, market manipulation, and unregistered entities. You can attach documents. The interface doesn’t feel like it was built in 2009.

Unfortunately, we never received an auto-acknowledgment email, so we had to manually create a screenshot to store our TCR number.

SEC complaint acknowledgement

For context on how seriously the SEC treats its reporting pipeline: the agency paid out over $600 million in whistleblower awards in FY2023, the highest single-year total since the program launched in 2011. That’s primarily for professional informants, not everyday consumers – but it shows institutional investment in the process.

CFTC (Commodity Futures Trading Commission)

The CFTC matters more than many people realize. Questionable forex trading platforms and crypto derivative schemes – two of the fastest-growing fraud categories – fall under its jurisdiction, not the SEC’s. Winvest’s model – AI-driven crypto trading with guaranteed daily returns, Bitcoin deposits, and no regulatory registration – sits squarely in CFTC territory as well as the FCA’s.

The reporting form works, but the user experience is noticeably less polished than the SEC’s. The dropdown categories are less intuitive, and the guidance text assumes more prior knowledge of financial regulation than most victims will have.

One standout feature: the CFTC’s whistleblower program offers eligible reporters 10–30% of sanctions over $1 million. For large-scale fraud, that’s a meaningful incentive – though it’s irrelevant for most everyday victims.

ASIC (Australian Securities and Investments Commission)

Australia has a structural problem that will confuse any victim trying to report: there are two separate reporting systems, and it’s not obvious which one applies to your situation.

When you navigate to ASIC’s scam reporting page and indicate that the issue occurred outside Australia, the page doesn’t offer a form. It redirects you to the International Organization of Securities Commissions (IOSCO) website, on the basis that possible cross-border investment fraud falls outside ASIC’s direct remit. As a result, we did not complete an ASIC reporting form – because the page itself told us not to.

That’s a significant finding. Winvest is not an Australian-registered entity, has no ASIC authorization, and is actively accessible to Australian investors. Yet a victim trying to report it through ASIC’s own website would hit a dead end, be pointed offshore, and likely never file a single detail.

For completeness, ASIC’s domestic reporting is separated into two systems. ASIC handles complaints about licensed entities, and ScamWatch – run by the ACCC – handles general scam reports. Australian victims of unlicensed operators typically end up needing both, with neither agency linking clearly to the other on first contact.

CySEC (Cyprus Securities and Exchange Commission)

CySEC matters to this test for a specific reason: Cyprus is one of the most common jurisdictions used by investment platforms targeting European retail investors.

Many questionable brokers and investment schemes either claim CySEC regulation as a badge of credibility or operate in the EU single market using Cyprus as a regulatory base. Checking whether a firm is on CySEC’s register – and reporting one that isn’t – should be straightforward. It isn’t quite.

The CySEC website has a consumer complaint form, but reaching it from the homepage requires navigating through several layers of menus that weren’t designed with a distressed victim in mind. There’s no prominent “report a scam” button.

The form itself is basic yet functional, but it can’t be completed anonymously, which adds an unnecessary barrier.

CySEC does maintain a public register of authorized firms and a list of warnings about unauthorized entities – both genuinely useful. But neither is prominently linked from the complaint journey.

Winvest does not appear on CySEC’s register of authorized investment firms.

MAS (Monetary Authority of Singapore)

MAS is widely regarded as one of Asia’s most rigorous financial regulators. But when it comes to reporting a suspicious financial platform directly, it doesn’t operate the way you’d expect.

The MAS website has no dedicated scam reporting form. Instead, it directs consumers to two external options: file a report with the Singapore Police Force, or visit ScamShield – a platform run by the National Crime Prevention Council. MAS itself does not accept or process individual scam reports from members of the public, unlike the SEC’s TCR portal or the FCA’s reporting form.

That’s an important distinction. MAS functions as a licensing and enforcement body, not a consumer reporting destination. For a victim (or a researcher running a test like this) there’s no form to submit, no reference number to receive, and no direct pipeline from a member of the public to MAS’s regulatory machinery.

ScamShield is a functional consumer tool, and the Singapore Police Force has a dedicated anti-scam command. So the infrastructure exists – it’s just fragmented across agencies in a way that requires a victim to already know which door to knock on.

Winvest does not appear on the Investor Alert List – a public register of unregulated entities that MAS updates and publishes separately. That list is useful for due diligence, but finding and checking it is a separate task from reporting a possible scam, and the two journeys aren’t connected on the MAS website.

The Overall Scoreboard

All testing was conducted simultaneously, with identical evidence submitted to each regulator on the same day. Scores reflect the reporting experience as we found it at the time of this investigation.

Make Full Width| Regulator | Total Score (/60) | Grade |

|---|---|---|

| SEC | 47 | A |

| FCA | 44 | B+ |

| CFTC | 34 | C |

| CySEC | 30 | C– |

| MAS | 6/40* | N/A |

| ASIC | 4/40** | N/A |

*MAS has no consumer scam reporting form. Reporters are directed to the Singapore Police Force or ScamShield.

**ASIC redirected international reporters to IOSCO. No form was completed.

The SEC stands out as the clear leader – a clean portal, anonymous submission, logical fraud categories, and immediate confirmation. The FCA and CFTC occupy the middle ground, functional but with hurdles that would cause many victims to give up partway through.

CySEC scores lowest among the regulators that offer a complete reporting journey. Both MAS and ASIC proved impossible to fully test: MAS because it has no consumer-facing form, and ASIC because it actively redirected international reporters away from its reporting page before they could file anything.

The Five Regulation Gaps That Operators Exploit

Gap 1 – Jurisdiction Vacuum

A platform registered in Argentina, claiming a New York address, with no FCA, SEC, CFTC, ASIC, CySEC, or MAS authorization, advertising to users globally: which regulator owns it?

In practice, none fully do. Cross-border coordination between these agencies exists on paper. At the consumer level, it doesn’t function in real time.

Gap 2 – No Single Reporting Portal

Of the four regulators that offered a complete reporting journey in our tests, none link to any of the others. The FCA requires UK victims to navigate a separate journey to a separate form. CySEC’s complaint process is designed for industry professionals, not distressed consumers. The SEC comes closest to a universal model – but it’s a US agency with a US mandate. Both MAS and ASIC route international reporters away from their own systems before a form is even reached.

A victim trying to report to all six regulators in one sitting would encounter four separate forms, two dead ends, and no signposting between them.

Gap 3 – Scams Outlive Response Times

Lifespans of investment scam websites can be as little as a few weeks. The average regulatory acknowledgment time is 5–10 business days, while actual enforcement action can take far longer. The arithmetic favors the scammer.

Gap 4 – Inconsistent Anonymous Reporting

The SEC allows full anonymity, as does the CTFC. CySEC’s form requests your personal details upfront.

For victims who are ashamed, or witnesses who have professional concerns about coming forward, this inconsistency is a barrier that costs the system real intelligence.

Gap 5 – No Feedback

Once you file a report with most of the regulators we tested, your submission is seemingly sent to a black box. There’s no case dashboard, no status update, no acknowledgment that anything happened beyond a reference number.

The FCA was the exception – the 2-minute acknowledgment with a case reference was the most transparent process we encountered. The rest need to catch up.

What Good Actually Looks Like

Two regulators stood out in our test: the SEC and the FCA. Both for different reasons.

The SEC’s TCR portal is the best pure reporting tool we encountered. Clean interface, anonymous submission, granular fraud categories, and immediate confirmation with a reference number. It was built for a consumer who knows something is wrong but doesn’t know the legal language for it. That’s the right design assumption.

The FCA was the only regulator in our test to acknowledge our complaint with an immediate follow-up email – a direct response confirming the report had been received and was under review. That kind of prompt acknowledgment matters. For a victim who has just gone through the effort of documenting a concerning platform or experience, and filing a report, hearing nothing for days compounds the sense that nothing will come of it. The FCA got that part right.

Singapore’s approach is worth noting separately. MAS doesn’t handle consumer reports about questionable financial platforms directly – but it has built a parallel infrastructure that does. ScamShield is a dedicated reporting and awareness platform, and Singapore’s Police Force runs a dedicated anti-scam command. The MAS Investor Alert List is searchable, regularly updated, and written in plain language. The pieces are there – they’re just not unified into a single consumer journey like the SEC’s portal.

Australia’s ScamWatch publishes a live public tracker showing reported losses by category, updated regularly. The ASIC/ScamWatch split creates genuine confusion for victims, but the ScamWatch data dashboard creates a degree of public accountability that most regulators lack.

What the best-designed systems share: a URL that’s easy to find, immediate acknowledgment, and some degree of public visibility into outcomes. None of it is technically complicated. It’s a question of institutional will.

CALLOUT: The APP Fraud Rule Change You Need To Know About

If you’ve been scammed via a bank transfer in the UK, there was a significant change that came in on 7 October, 2024, that you should know about.

Rules from the Payment Systems Regulator (PSR) require UK banks and payment firms to reimburse victims of Authorised Push Payment (APP) fraud – where you were tricked into sending money to a scammer’s account.

The maximum reimbursement is £85,000. Both the sending and receiving banks share liability for the refund. You must report the fraud to your bank promptly. Banks can apply a claim excess of up to £100 for standard customers (this doesn’t apply to vulnerable customers).

This is the most significant shift in UK fraud victim protection in a decade. It doesn’t apply to investment losses held in potentially fake trading platforms – only to direct bank transfers made to fraudsters. But for the most common type of investment scam (where victims are instructed to transfer funds directly), it creates a meaningful route to recovery that didn’t exist before October 2024.

What to do: Report to your bank within 13 months of the last payment. Keep all communication records. If your bank refuses to reimburse, escalate to the Financial Ombudsman Service (FOS) – it’s free to use and has binding power.

What To Do If You’ve Been Targeted

If you think you’ve encountered a suspicious investment platform – whether or not you’ve lost money – here’s how to respond:

- Call your bank immediately. If you’ve transferred money, call the number on the back of your card. Speed matters.

- Report to your national regulator. In the UK, that’s the FCA and Action Fraud. In the US, file with both the SEC and CFTC. In Australia, use ScamWatch. In Singapore, report to ScamShield. In Cyprus and across the EU, use CySEC. Filing in multiple jurisdictions increases the likelihood that the report reaches someone with the authority to act.

- Preserve everything. Screenshots, transaction IDs, email threads, wallet addresses. If crypto was involved, submit the wallet address to Chainabuse – it feeds into a shared database used by blockchain analytics firms and law enforcement.

- Archive the evidence. Dodgy websites frequently alter or delete content once scrutiny increases. Use the Wayback Machine to create a timestamped snapshot of any suspicious platform before it disappears.

- Get support. Fraud victims frequently experience shame, stress, and real financial trauma. In the UK, Victim Support and Citizens Advice both offer free help. Neither requires you to have filed a police report first.

The Bottom Line

Our hands-on tests shows that reporting a suspicious investment platform is harder than it should be.

The system is fragmented across regulators in different jurisdictions – none of which communicate with each other in real time at the consumer reporting level.

Of the six we tested, only four offered a complete reporting journey. ASIC redirected us away before we could file anything. MAS has no consumer form at all – it points you to the police or a separate government website.

The SEC is the clear standout: a clean portal, anonymous submissions, and immediate confirmation. The FCA and CFTC are functional but friction-heavy. CySEC scores lowest among the regulators that offer a full process.

Most worryingly, not a single regulator that we reported Winvest to appear to have taken any action against the firm. At least we’ve not had any communication from regulators to confirm it’s being looked into, nor is the firm on any of the regulators’ warning lists.

None of this means reporting is pointless. Volume matters. Every report filed contributes to a dataset that eventually informs enforcement action, even when individual outcomes are invisible.

But the burden right now falls almost entirely on victims and witnesses. That’s the wrong way round.

Editorial Note

This report presents the findings and opinions of our research team based on publicly available information, materials displayed on the Winvest website, and searches of the regulatory databases mentioned. References to “warning signs,” “red flags,” or matters that appear “suspicious” express our assessment and do not constitute a legal finding that Winvest, its operator or any associated person has committed fraud, operated a scam or breached any law.

We were unable to independently verify some claims made by Winvest or confirm a matching regulatory license through the registers we searched. This does not prove that all its claims are false, that no relevant authorisation exists, or that any regulator has declined to take action. Regulatory reviews and subsequent decisions may not always be disclosed publicly.

Based on the unusually high advertised returns, questionable marketing, third-party reviews, information we were unable to verify, and the lack of regulatory approvals described, we do not recommend depositing funds with Winvest. Readers should conduct their own due diligence and seek qualified financial or legal advice before making any investment decision.

Winvest has been contacted and invited to respond to our detailed findings. No substantive response had currently been received by Winvest. Should they respond, we will review credible supporting evidence and correct any material factual errors as appropriate.