The Subscription Economy Is Quietly Draining Your Household Wealth

Christian Harris

Christian is a seasoned analyst, leveraging his expertise in stocks, forex, and crypto to evaluate brokers worldwide. With hands-on trading experience and a strong focus on risk management, he helps traders find reliable platforms. Christian's work for BrokerListings.com has been cited in the Financial Times.

Christian Harris Profile PageTobias Robinson

Tobias is committed to helping traders find the right brokerage for their needs. He has tested 200+ brokers, spent 2,600+ hours using different platforms, and placed 2,100+ trades.

Tobias Robinson Profile PageJames Barra

James is an experienced broker analyst with a background in financial services. He has spent 2,500+ hours testing brokers, used 35+ different platforms and apps, audited 120+ broker T&Cs, and verified 300+ regulatory licenses. James has also been on US and UK TV news channels discussing reports conducted by BrokerListings.com and sharing his expertise.

James Barra Profile PageApril 8, 2026

Melissa Carter (not a real person) noticed her bank balance seemed off – slightly lower than expected. After dinner, with her kids doing homework and her husband, Aaron (also fictional), watching TV, she opened her banking app to investigate.The charges arose one after another in a steady rhythm. $14.99. $9.99. $15.99. $12.99. $10.99. Most stood out – a streaming service the family enjoyed on weekends, a music subscription, cloud storage, and a meal-kit plan that became indispensable during hectic weeks. None of these individual charges seemed alarming. Each one appeared entirely justifiable.

But when Melissa finished tallying them, the total stopped her cold – and led her to reconsider just how those charges had quietly multiplied.

Twenty-four separate recurring subscriptions. About $350 per month. Over the course of a year, that adds up to $4,200.

Melissa and her husband, Aaron, live in Columbus, Ohio, with their two children. Aaron works in warehouse logistics, and Melissa is a dental assistant. Their combined household income sits at around $76,000 a year, which, after federal taxes, payroll deductions, and health insurance premiums, translates to roughly $60,000 in take-home pay.

Their subscription costs now consume about 7% of that. The Carters are, by any metric, prudent with money. They grab store brands at the grocery store without hesitation. They refinanced their mortgage when rates dipped and felt confident about it. Their SUV is seven years old, with no plans to replace it. They don’t view themselves as lavish spenders.

And yet, the subscription stack grew anyway – quietly, incrementally, one seemingly reasonable service at a time. A streaming platform here. A productivity tool there. A digital fitness app. A gaming pass for their son. A premium cloud storage plan that got added when they ran out of space for family photos.

Like silt blanketing a riverbed, the charges accrued so subtly that the sum vanished from notice – until someone investigated.

Key Takeaways

- Subscriptions now absorb a meaningful share of household income. A typical middle-income household can spend around $4,000+ per year on recurring services, including streaming, software, retail memberships, and apps. For many families, this amounts to roughly 5–8% of take-home income, a share comparable to what households save each year.

- Small monthly payments hide high long-term costs. A household spending $350 per month on subscriptions could accumulate about $182,000 over 20 years at a 7% annual return if that money were invested instead. Even modest subscription stacks can translate into six-figure opportunity costs over time.

- Most people underestimate how much they spend. Consumers often misjudge their subscription spending by a wide margin. One study found people believed they were paying about $86 per month, when the actual average was around $219—a gap of more than $1,500 per year.

- The subscription economy has grown into a massive global market. Recurring-revenue services have expanded rapidly across media, software, retail, and fintech. The global subscription economy is projected to reach more than $2 trillion in annual revenue within the next decade, reflecting a major shift toward recurring billing models.

- Many households are paying for services they don’t use. Research suggests over 85% of consumers have at least one unused subscription, wasting roughly $300–$400 per year on services that go largely unused.

How We Got Here

To understand how a family like the Carters ends up spending $350 a month on digital services without quite noticing, it helps to look at how dramatically consumer spending has changed over the past 15 years or so.

What happened wasn’t a sudden transformation – it was a slow migration from ownership to access, driven by a handful of enormously successful companies that figured out something important: a small monthly fee is psychologically far easier to accept than a large one-time payment, and automatic renewal means you only have to win a customer’s approval once.

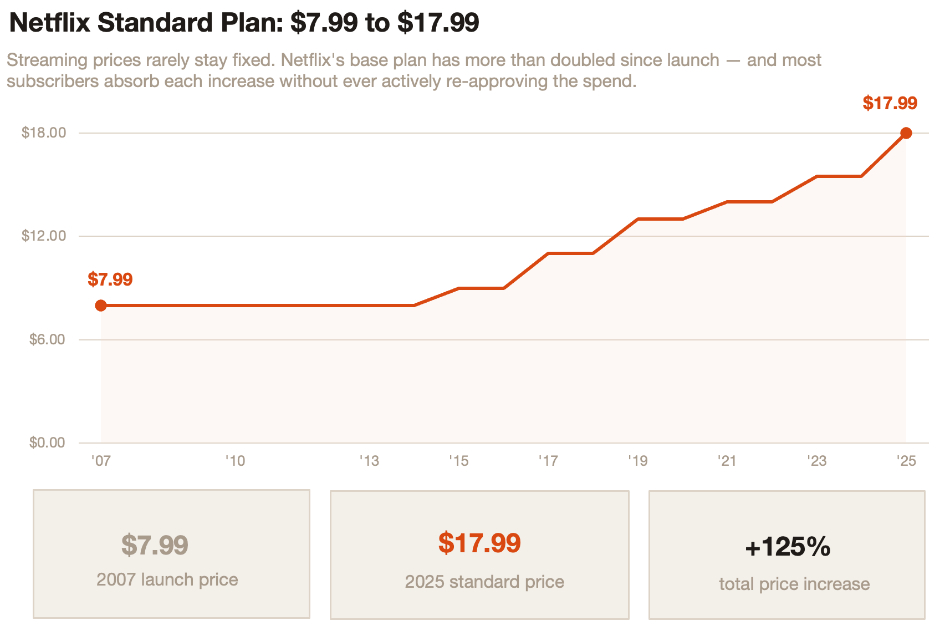

Netflix was arguably the company that proved the model could scale. When it launched streaming in 2007, a subscription cost around $8 a month – barely the price of a fast-food lunch. Spotify did the same thing for music, replacing the iTunes model of paying per song or album with an all-you-can-listen monthly membership.

Microsoft converted its Office suite into Microsoft 365. Adobe, rather than selling Photoshop for hundreds of dollars upfront, shifted to Creative Cloud and began charging a monthly fee. Amazon bundled shipping benefits, video streaming, music, and a growing list of other perks under a single Prime membership.

Each of these moves was logical in isolation. Together, they rewired how people conceive of paying for things.

The brilliance – or, depending on your view, the slyness – of the subscription model lies in how it reshapes decisions.

A traditional purchase requires a conscious choice at the moment of payment. You hand over $200 for a piece of software and feel that cost. A $15 monthly subscription barely registers. And once it’s set up, it requires no further decisions. It just continues, month after month, drawing down your account while you think about other things.

Price increases slide through the same way. Netflix has raised its rates repeatedly over the years, and most subscribers absorb those increases without ever formally deciding they’re still getting enough value to justify the new price. The subscription just renews, a few dollars more expensive than before, and life goes on.

The Numbers Behind The Pattern

To get a clearer picture of how subscription spending weighs on households at different income levels, it’s useful to think about what financial analysts sometimes call a ‘Subscription Load Ratio’ – simply the share of after-tax income that goes toward recurring services.

When you model this across different income tiers using Census household income data and current pricing for common digital subscriptions, a consistent and somewhat uncomfortable pattern emerges.

Households in the bottom income quintile, with around $30,000 in after-tax income, spend roughly $2,400 a year on subscriptions – a load of about 8% of take-home pay. Lower-middle-income households earning around $45,000 carry a load of about 7.3%.

Median household incomes, like the Carters’, land right around 7%. Upper-middle and high-income households spend more in absolute terms – sometimes $5,000 to $7,000 a year – but because their incomes are larger, the proportional burden is smaller, around 5% to 6%.

Make Full Width| Income Tier | After-Tax Income | Annual Subscriptions | Subscription Load |

|---|---|---|---|

| Bottom 20% | $30,000 | $2,400 | 8.0% |

| Lower-Middle | $45,000 | $3,300 | 7.3% |

| Median Household | $60,000 | $4,200 | 7.0% |

| Upper-Middle | $90,000 | $5,400 | 6.0% |

| Top 20% | $135,000 | $7,200 | 5.3% |

What makes this pattern notable is the comparison it invites. According to the U.S. Bureau of Economic Analysis, the national personal savings rate has hovered somewhere between 3% and 6% in recent years.

This means that many American households now spend more on digital subscriptions than they save each month. As a result, subscriptions quietly absorb resources that could otherwise build wealth, competing with savings goals even if they don’t cause a budget crisis.

These figures exclude housing, utilities, insurance, and other unavoidable costs. The focus here is strictly the discretionary layer – streaming services, software subscriptions, fitness apps, gaming passes, membership programs, and similar services that households adopt and seldom review.

The Hidden Cost Of Convenience

None of this means subscriptions are inherently wasteful. That’s an important distinction. Many of them replace things that cost more.

A streaming service often undercuts what a cable package used to cost. A music subscription makes buying individual albums look absurd by comparison. Cloud storage is cheaper and more reliable than external hard drives. Some software subscriptions – Adobe’s tools, say, or Microsoft 365 – are professionally essential for the people who use them, generating income that far exceeds the monthly fee.

The issue is not whether subscriptions offer value – most do. The real impact comes from how they can accumulate and divert a meaningful portion of a household’s income without conscious oversight, gradually reducing funds available for other financial goals.

Industry tactics are blunt. A $12 monthly fee elicits far less psychological resistance than a $144 annual bill would, though they add up to the same amount.

Bundling makes it hard to evaluate individual value. Amazon Prime is a perfect example, wrapping so many different services into one fee that it becomes nearly impossible to decide whether any single component justifies the cost.

The opt-out nature of automatic renewal ensures inertia, not active approval, sustains most subscriptions. You chose to sign up. You must choose to cancel. Yet the cancellation decision never reaches the top of the priority list.

This is exacerbated by what could be called subscription creep – the habit of adding new services without discarding old ones.

The family gets Disney+ for a specific series. The series ends, but the subscription doesn’t. A pandemic-era fitness app gets replaced by a gym membership, but the app keeps billing. A trial period converts to a paid plan because canceling requires navigating an app no one uses anymore.

Each oversight is tiny. Collectively, they amount to a stack that few households could recall.

What It Really Costs Over Time

The real impact of subscription spending is best understood in terms of opportunity cost – the alternative uses for that money if it were allocated elsewhere, such as toward long-term financial growth.

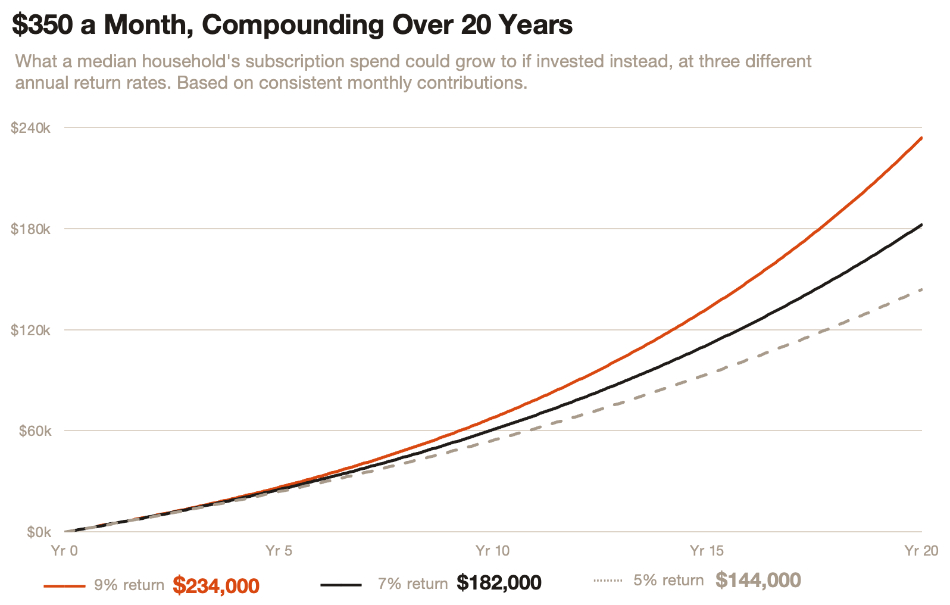

The Carters spend $350 a month on subscriptions. That’s not an unusual amount for a middle-income household with two kids. It doesn’t feel like a lot. But run that figure through the math of compound investment returns, and the picture changes considerably.

If that $350 were invested monthly instead – assuming a 7% average annual return, consistent with long-term stock market performance- it would compound to around $182,000 over 20 years. At 9%, the figure swells to about $234,000. Even with a conservative 5%, you’re still looking at roughly $144,000.

| Annual Return | Future Value |

|---|---|

| 5% | $144,000 |

| 7% | $182,000 |

| 9% | $234,000 |

This approach shows how subscription costs, often overlooked, can significantly diminish household wealth over time by redirecting money that could otherwise go toward consistent saving and compound growth.

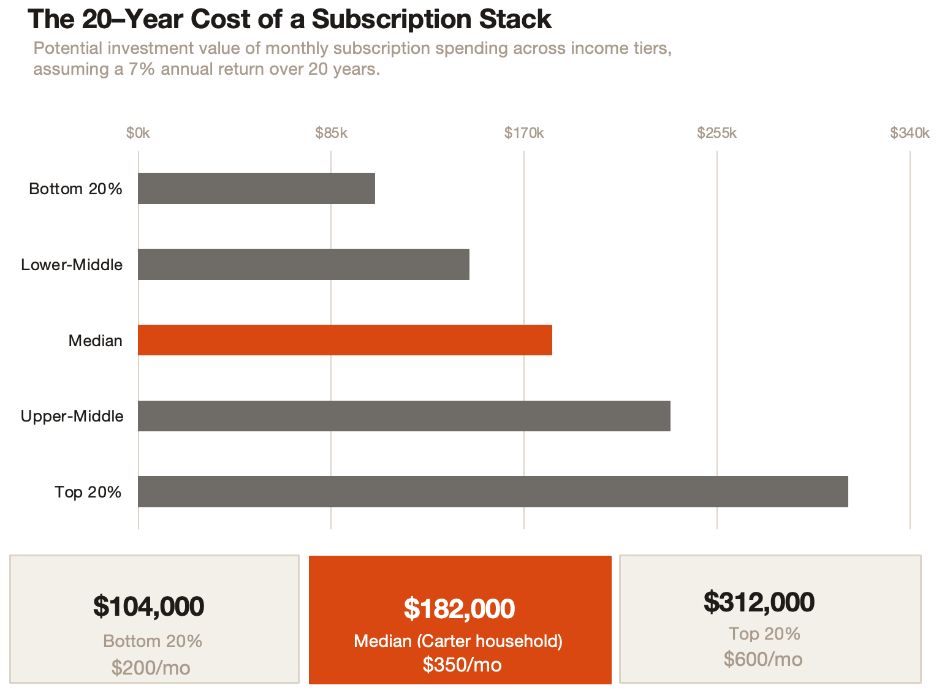

The comparison is even starker when you extend it across income levels. A household in the bottom income quintile spending $200 a month on subscriptions – already a meaningful burden relative to their income – could theoretically accumulate around $104,000 over 20 years at 7%. A higher-income household spending $600 a month could be looking at more than $300,000.

| Income Tier | Monthly Subscriptions | 20-Year Value at 7% |

|---|---|---|

| Bottom 20% | $200 | $104,000 |

| Lower-Middle | $275 | $143,000 |

| Median | $350 | $182,000 |

| Upper-Middle | $450 | $234,000 |

| Top 20% | $600 | $312,000 |

These figures aren’t predictions, and they’re not meant to imply that every dollar currently going to Netflix should be rerouted to a brokerage account. But they do put a concrete number on what’s sometimes called the opportunity cost of recurring spending – the wealth that isn’t being built because money is flowing out steadily in small, invisible increments.

For a median household, $182,000 is a significant retirement cushion. It’s college tuition. It’s the difference between financial fragility and financial security in a genuine emergency. The fact that it’s disappearing into a collection of $10 and $15 monthly charges doesn’t make it less real.

Subscriptions In The Broader Financial Picture

It would be unfair to treat subscription spending as the primary culprit in household financial stress. Families face serious pressures across housing, healthcare, food, and transportation that dwarf the scale of the subscription stack.

According to the Federal Reserve, total U.S. household debt now exceeds $17 trillion, and credit card balances alone recently crossed $1 trillion. Against that backdrop, a few hundred dollars a month in streaming and software fees might seem like a rounding error.

But subscriptions interact with those larger pressures in ways that matter. Every fixed monthly commitment reduces financial flexibility.

For households already operating close to the edge of their budgets, a dense subscription stack means less room to absorb an unexpected expense, less capacity to direct money toward debt repayment, and less ability to respond to the kind of financial shocks – a car repair, a medical bill, a job disruption – that can quickly become crises for families without adequate savings.

The subscription economy didn’t create household financial vulnerability, but it quietly deepens it for millions of families who have never sat down and done the math the way Melissa Carter did that Tuesday night.

The Bigger Shift

There’s a philosophical dimension to all of this that goes beyond the dollars. The subscription economy represents a fundamental change in the relationship between consumers and the things they use.

For most of human commercial history, buying something meant owning it. You paid once; it was yours. The subscription model quietly reverses that logic. You never really own anything. You license access to it, month by month, and that access can be revoked if you stop paying – or if the company decides to raise prices, change terms, or discontinue the service entirely.

What once sat on a shelf, permanent and paid for, now lives in the cloud, tethered to a recurring charge.

This isn’t inherently sinister, but it does mean that the ongoing costs of modern digital life are more open-ended than previous generations of consumers ever experienced.

There’s no point at which your subscription stack is “paid off.” It simply continues, a permanent overhead attached to the life you’ve built around it. And because it grows incrementally rather than arriving as a single bill, it rarely prompts the kind of deliberate reckoning that a major purchase would.

The Quiet Drain

When Melissa Carter closes her banking app, she isn’t planning a dramatic overhaul. Some of those subscriptions are genuinely worth it – the streaming the family actually watches, the cloud storage keeping years of photos safe, the meal kits that make Wednesday nights survivable.

But knowing the total changes something. The $350 a month that felt abstract before now has a shape. Over 20 years, at a reasonable rate of return, it becomes $182,000.

That figure doesn’t feel like streaming movies or storing files. It feels like something else entirely – an education fund, a retirement top-up, a cushion against the kind of unexpected disaster that can upend a family’s finances in an afternoon.

The subscription economy didn’t transform household spending through dramatic moments of decision. It did it through accumulation, through the patient multiplication of small, reasonable-seeming charges that arrive quietly and leave just as quietly, month after month, year after year.

The drain isn’t dramatic. It doesn’t announce itself. It just persists, a slow and steady current running just beneath the surface of the household budget, reshaping what’s possible over time in ways that most families never quite stop to calculate.

Until one Tuesday night after dinner, someone finally does.