Best Brokers With Custodial Accounts 2026

Discover our top brokers offering custodial accounts for minors, designed to give parents secure control over a child’s financial future, with trusted investment tools.

Paul Holmes

With over 15 years of trading experience, including developing algorithmic strategies on MetaTrader and evaluating brokers, he brings deep expertise in market analysis and trader education, helping traders choose the right platform for their requirements.

Paul Holmes Profile PageTobias Robinson

Tobias is committed to helping traders find the right brokerage for their needs. He has tested 200+ brokers, spent 2,600+ hours using different platforms, and placed 2,100+ trades.

Tobias Robinson Profile PageJames Barra

James is an experienced broker analyst with a background in financial services. He has spent 2,500+ hours testing brokers, used 35+ different platforms and apps, audited 120+ broker T&Cs, and verified 300+ regulatory licenses.

James Barra Profile PageFebruary 23, 2026

-

1Firstrade is a US-based discount broker-dealer authorized by the SEC and a member of FINRA/SIPC. It offers welcome bonuses, advanced tools and apps, and commission-free trading. Firstrade Securities is a popular top online brokerage, and opening a new account is fast and simple.

Compare The Best Brokers Offering Custodial Accounts For Minors

We reviewed the top brokers that offer custodial accounts - here’s how they compare across key features:

| Broker | USD Account |

Demo Account |

Minimum Deposit |

Minimum Trade |

Leverage |

Copy Trading |

Regulator |

Instruments |

Platforms |

Account Currencies |

Automated Trading |

AI |

Guaranteed Stop Loss |

|

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ✓ | ✗ | $0 | $1 | ✗ | ✗ | SEC, FINRA | Stocks, ETFs, Options, Mutual Funds, Bonds, Cryptos, Fixed | Firstrade Invest 3.0, TradingCentral | USD | ✗ | ✗ | ✗ | ||

| Broker | USD Account |

Demo Account |

Minimum Deposit |

Minimum Trade |

Leverage |

Copy Trading |

Regulator |

Instruments |

Platforms |

Account Currencies |

Automated Trading |

AI |

Guaranteed Stop Loss |

How Safe Are The Top Custodial Account Brokers?

Custodial accounts involve long-term investing for a child’s future. Here's how the best brokers ensure account safety:

| Broker | Trust Rating |

Guaranteed Stop Loss |

Negative Balance Protection |

Segregated Accounts |

|---|---|---|---|---|

| ✗ | ✗ | ✗ | ||

| Broker | Trust Rating |

Guaranteed Stop Loss |

Negative Balance Protection |

Segregated Accounts |

Managing Custodial Accounts On Mobile

Need to access and manage your child’s custodial account on the go? See how these brokers perform on mobile apps:

| Broker | Mobile Apps |

iOS Rating |

Android Rating |

Smart Watch App |

|---|---|---|---|---|

| iOS & Android | ✗ | |||

| Broker | Mobile Apps |

iOS Rating |

Android Rating |

Smart Watch App |

Are The Top Custodial Account Brokers Good For Beginners?

If you're setting up your first custodial account, here's how these brokers offer guidance, educational resources, and user-friendly tools:

| Broker | Demo Account |

Minimum Deposit |

Minimum Trade |

Education Rating |

Support Rating |

Fractional Shares |

Demo Competitions |

|---|---|---|---|---|---|---|---|

| ✗ | $0 | $1 | ✓ | ✗ | |||

| Broker | Demo Account |

Minimum Deposit |

Minimum Trade |

Education Rating |

Support Rating |

Fractional Shares |

Demo Competitions |

Are The Top Custodial Accounts Suitable For Experienced Investors?

Here’s how top brokers meet the needs of seasoned traders:

| Broker | Automated Trading |

VPS |

API |

AI |

Pro Account |

Leverage |

Low Latency |

Extended Hours |

|---|---|---|---|---|---|---|---|---|

| ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | |

| Broker | Automated Trading |

VPS |

API |

AI |

Pro Account |

Leverage |

Low Latency |

Extended Hours |

Accounts Comparison

Compare the trading accounts offered by Best Brokers With Custodial Accounts 2026.

| Broker | Demo Account |

Interest on Cash |

Islamic Account |

Joint Account |

Managed Account |

PAMM |

MAM |

LAMM |

Pro Account |

|---|---|---|---|---|---|---|---|---|---|

| ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | |

| Broker | Demo Account |

Interest on Cash |

Islamic Account |

Joint Account |

Managed Account |

PAMM |

MAM |

LAMM |

Pro Account |

Detailed Ratings: Best Brokers For Custodial Accounts

Explore how each broker offering custodial accounts scored in our independent rating system:

| Broker | Trust |

Platforms |

Assets |

Mobile |

Fees |

Accounts |

Research |

Education |

Support |

|---|---|---|---|---|---|---|---|---|---|

| Broker | Trust |

Platforms |

Assets |

Mobile |

Fees |

Accounts |

Research |

Education |

Support |

Compare Fees At Brokers Offering Custodial Accounts

We analyzed trading fees and administrative costs to find the most cost-effective custodial account brokers for minors:

| Broker | Cost Rating |

Fixed Spreads |

Inactivity Fee |

EUR/USD Spread |

Crypto Spread |

|---|---|---|---|---|---|

| ✗ | $0 | ✗ | Variable | ||

| Broker | Cost Rating |

Fixed Spreads |

Inactivity Fee |

EUR/USD Spread |

Crypto Spread |

Why Trade With Firstrade?

Firstrade is ideal for beginners wanting to trade US stocks without commission fees. It offers plenty of free educational resources and high-quality research, including its new FirstradeGPT tool. Users also get trading ideas from Morningstar, Briefing.com, Zacks, and Benzinga.

Pros

- FirstradeGPT ranks among the initial brokers to offer AI-powered analysis.

- In 2025, Firstrade Invest 3.0 will enhance the platform with a cleaner interface and faster order entry, benefiting active traders in key areas such as watchlists and options chains.

- Improved stock trading features now include overnight trading and fractional shares.

Cons

- Customer support needs improvement after testing, with no 24/7 help available.

- Over 90% of the evaluated options lack a demo or paper trading account.

- Firstrade emphasizes stocks and lacks forex options, reducing diversification opportunities.

Filters

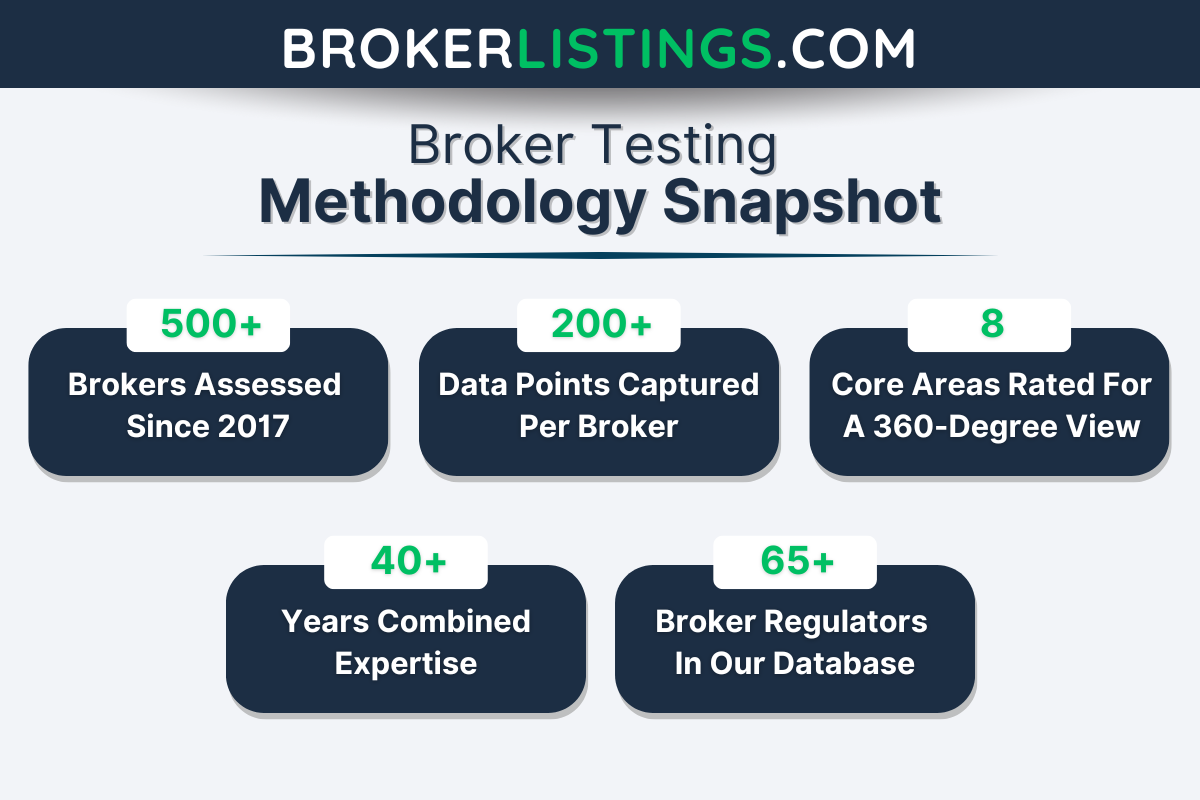

How BrokerListings.com Chose The Best Brokers With Custodial Accounts

We selected the best custodial account brokers based on over 200 data points, including account setup simplicity, investment choices, educational tools, fee structures, and long-term support for minor-owned assets.

Each broker on our list supports custodial accounts, allowing parents or guardians to invest on behalf of a child. Assets in these accounts often legally belong to the minor and transfer to them once they reach the age of majority – typically 18 or 21, depending on the country and respective laws.

What To Look For In a Custodial Account Broker

No-Nonsense Fees: What You’ll Pay to Open and Keep the Account

When choosing a custodial account, the first thing we always dig into is the cost, and for good reason. Some brokers charge sneaky setup fees, others chip away with monthly maintenance costs, and a few hit you with both. For long-term investing, especially when you’re managing money on behalf of a minor, those little fees can add up fast.

Based on our assessments of the best trading accounts, we look at two key criteria here:

- Account Opening Charges: Is there a setup fee or minimum deposit requirement?

- Ongoing Maintenance Fees: Are there monthly, annual, or inactivity fees you’ll need to keep track of?

From our tests and account reviews, we found that fee structures vary wildly. Some brokers push high fees under the guise of premium service. We don’t buy that – and neither should you.

Top Pick: Firstrade has one of the most straightforward and cost-friendly custodial account offerings we’ve seen. There’s no fee to open the account, no minimum deposit, and – best of all – no annual or maintenance charges. That makes it especially appealing for parents or guardians setting up long-term investments without wanting to lose money to overheads.

We opened a custodial account with Firstrade ourselves and were pleasantly surprised at how quick and transparent the entire process was. There were no hidden clauses or onboarding friction. You fill out a simple form, link a funding source, and you’re in.

Investment Options That Grow with Your Family

When setting up a custodial account, you’re not just parking money – you’re planting seeds. So the range of investment options matters a lot.

Whether you’re planning to hand over the account when your child turns 18 or 21, or you’re building a foundation for their financial future, you want flexibility and choice.

We always look at three big things in this area:

- Access to U.S. stocks, ETFs, and mutual funds

- Commission policies and trading flexibility

- Long-term investment tools that support a buy-and-hold strategy

Some brokers limit the selection or tack on trading fees that quietly erode returns over the years. That’s where our evaluations come in – we dig into the details, not just the marketing headlines.

Top Pick: Firstrade stands out for offering a wide range of investment options with zero trading commissions, which is a game-changer for custodial accounts. You get access to:

- Stocks listed on major U.S. exchanges

- Exchange-Traded Funds (ETFs) across all sectors

- Over 11,000 mutual funds

- Options trading, though not typically used in custodial accounts, is available when the account transitions.

We tested the platform’s search and filter functions ourselves, and it was easy to drill down by asset class, fund family, performance, and risk profile. That’s especially helpful if you’re managing a long-term strategy – whether it’s targeting tech growth, dividend-paying blue chips, or balanced mutual funds.

Ease of Use: Platform That Works for Parents and Teens

Even the best investment platform isn’t worth much if it’s a headache to use. With custodial accounts, you’ve got two users to think about: the adult managing the account and the future adult who’ll eventually take it over. That’s why we always test the platform from both angles.

For this section, we focus on:

- How intuitive the sign-up and dashboard experience is

- How easy it is to make deposits, place trades, and check performance

- Whether it’s friendly enough for teens to learn the ropes later on

Many brokers design platforms for serious traders and professionals, that’s fine if you’re day trading – not so great if you’re a parent just trying to make smart, consistent decisions for your child’s future.

Top Pick: In our hands-on review, we found Firstrade‘s interface to be one of the easiest to navigate. From setting up the custodial account to placing the first trade, everything was laid out in plain English, with no jargon traps or cluttered menus.

The dashboard is clean and well-organized, making it easy to track holdings, dividends, and account performance at a glance. You don’t need to be a seasoned investor to understand what’s happening – and that’s exactly the point.

We think that’s especially important when you’re planning to pass the account over to your child down the line. It sets them up with something they can confidently manage, not something intimidating.

Tax Docs, Gifting Rules, and the Essential Admin

It’s not the flashiest part of choosing a custodial account, but it’s one of the most important. Taxes, gifting limits, and paperwork can trip up even well-intentioned investors if the broker doesn’t make things clear.

That’s why we check how well a platform handles the behind-the-scenes essentials – and how easy it is to stay on the right side of IRS rules.

Here’s what we look for:

- Clarity around annual gifting limits and IRS reporting thresholds

- Availability of tax forms like Form 1099

- Ease of tracking cost basis and gains for tax-time prep

- Built-in tools or help content for guardians managing multiple contributions

A strong custodial platform doesn’t just help you grow the account – it helps you manage the paperwork that comes with it.

Top Pick: Firstrade takes a refreshingly no-fuss approach to tax and compliance support. Every custodial account includes automatic access to key tax forms, like Form 1099-DIV (dividends), 1099-B (capital gains/losses), and 1099-INT (interest), depending on the assets you hold.

We checked our test account around tax season and found the downloadable forms right in the dashboard under the “Documents” tab. No hunting, no waiting for an email. They’re available by early February, and if you’re working with a tax preparer or software, they’re formatted for easy upload.

On the gifting side, Firstrade allows multiple contributions from different sources, which is ideal for families who want to involve grandparents or other relatives in building the account. You can also track contribution history easily within the account activity tab, which helps keep you under the annual IRS gift tax exclusion.

Education and Support: Hand-Holding When You Need It

Even if you’ve opened a few brokerage accounts before, a custodial account has its own learning curve. You’re managing money that technically belongs to someone else, and at some point, they’ll be the ones taking over.

That’s why we check how much help a broker offers, both in terms of customer support and educational resources.

Here’s what we look for:

- Responsiveness of support via phone, chat, or email

- Quality of beginner-focused investing education

- Help content geared toward custodians and minors

- Availability of onboarding help or live assistance if needed

Not everyone wants a hand to hold. But if you do? The right broker should have one ready.

Top Pick: Firstrade isn’t flashy with its support features, but it delivers where it counts. You get access to live customer service via phone and email, and in our tests, wait times were minimal.

We contacted support with a few basic questions about setting up a custodial account, gifting limits, and tax form timelines. The answers were clear, polite, and valuable, without trying to upsell anything.

On the education front, Firstrade offers a free, self-paced Learning Center with articles and explainers on stock market basics, mutual fund strategies, and portfolio building. It’s not gamified or overly branded like some larger platforms, but it’s practical and well-suited for parents who want to learn as they go or explain the basics to their kids later.

We especially like the glossary of investment terms, which keeps things understandable without dumbing it down. There’s also video content for more visual learners, though it’s a bit limited in depth.

Security and Peace of Mind: Is Your Child’s Money Safe?

When you’re opening a custodial account, you’re thinking long-term – years down the line, in some cases. That makes security, regulation, and account protection absolutely non-negotiable.

It’s not just about guarding against hackers or identity theft – it’s about making sure the broker follows industry rules, holds client funds safely, and treats your child’s money with the same care they’d treat your own.

Here’s what we assess:

- Regulatory oversight and broker licenses

- Securities Investor Protection Corporation (SIPC) coverage

- Data encryption and digital security practices

- Account activity alerts and transparency

A good custodial account gives you growth potential. A great one gives you sleep-at-night safety while it grows.

Top Pick: Firstrade ticks every major box when it comes to safety. They’re a registered broker-dealer and a member of both the Financial Industry Regulatory Authority (FINRA) and the Securities Investor Protection Corporation (SIPC).

That means your child’s account is backed by up to $500,000 in SIPC protection, including up to $250,000 in cash, in case the broker ever fails.

We also dug into Firstrade’s digital security policies. The platform uses 256-bit encryption, offers two-factor authentication (2FA), and sends real-time account alerts for logins and trade activity. It’s not cutting-edge in a Silicon Valley sense — but it’s safe, tested, and consistent.

And for parents who want to keep a close eye on what’s happening? Firstrade’s account activity logs and trade confirmations are easy to access, with full transaction transparency. No buried fees. No mystery trades. Just clean, readable records.